If a client, landlord, or general contractor has just asked you to “send over a COI,” they’re asking for a certificate of liability insurance, a one-page document that proves you carry business insurance. It sounds bureaucratic, and it is, but understanding it matters: the certificate itself gives the other party no coverage, and the single most expensive mistake in this area is confusing a certificate holder with an additional insured.

Most explanations either oversimplify this document (“it’s just proof of insurance”) or bury you in jargon. This guide does neither: it walks the ACORD 25 form line by line, puts real cost and timing numbers on getting one, and zeroes in on the single distinction, certificate holder versus additional insured, that actually decides whether anyone is protected. The goal is to make you the person in the room who genuinely understands the document everyone else just forwards.

What this guide covers

- What a certificate of liability insurance is

- The ACORD 25 form, line by line

- What a certificate is NOT

- Certificate holder vs. additional insured

- How to get a certificate

- What it costs

- Why businesses ask for one

- Certificates for common situations

- How to read and verify one

- When a certificate is wrong or expires

- Frequently asked questions

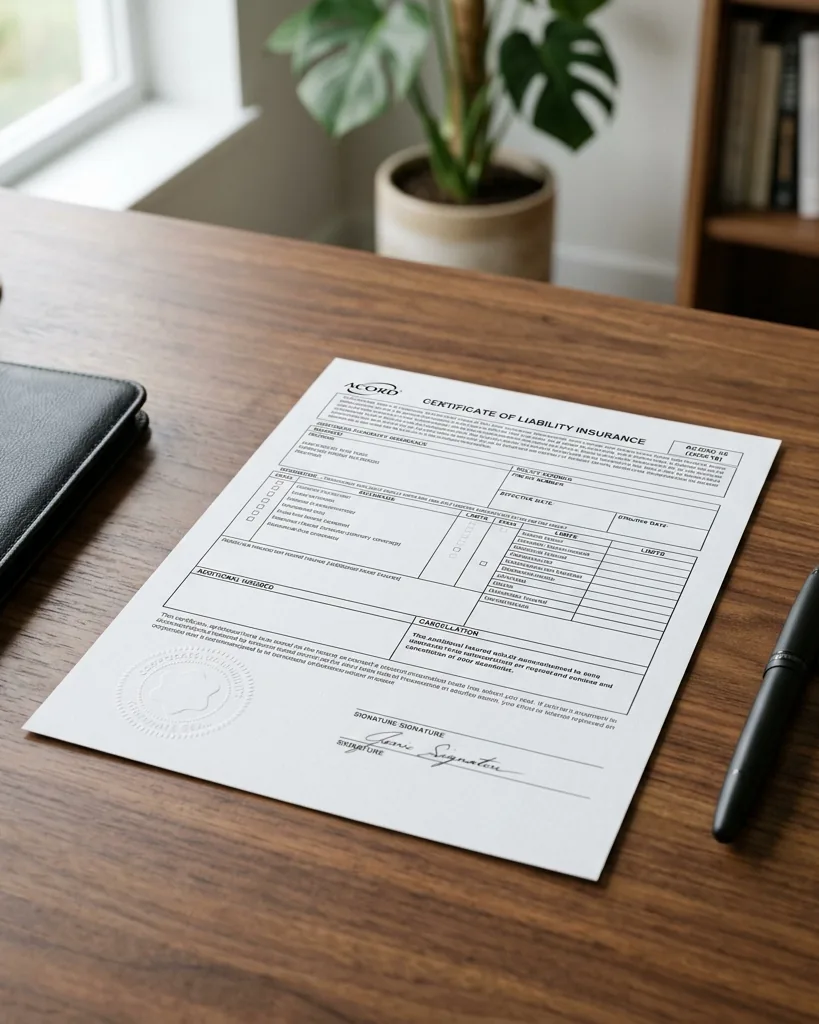

What a certificate of liability insurance is

A certificate of liability insurance is a standardized document that summarizes the key facts of your business insurance coverage on a single page. It exists so that one business can prove to another that it carries insurance, without having to hand over a hundred-page policy. The standard version is known as the ACORD 25 form, created and maintained by ACORD, the organization that sets standardized insurance forms used across the industry.

You’ll be asked for one constantly once you run a business. A landlord wants proof before handing you keys to a commercial space. A general contractor won’t let you on site without it. Corporate clients require it before signing. In each case, the other party wants reassurance that if something goes wrong, your insurance, not their pocket, will respond. The certificate is that reassurance in a form everyone in business recognizes at a glance.

The ACORD 25 form, line by line

The ACORD 25 packs a lot into one page. Once you know what each block means, you can read any certificate in seconds:

- The insured: Your business’s legal name and address, the party whose coverage the certificate describes.

- The producer: The insurance agency or broker that issued the certificate.

- The insurers: The actual insurance companies providing each coverage, each given a letter (A, B, C) referenced in the rows below.

- Types of coverage: Usually commercial general liability, commercial auto, umbrella or excess liability, and workers’ compensation, each with its own row.

- Policy numbers and dates: Each coverage shows its policy number plus an effective date and an expiration date.

- Limits: The dollar amounts the policy will pay, typically split into a per-occurrence limit (the most for a single claim) and an aggregate limit (the most for the whole policy period).

- Description of operations: A free-text box noting contract details, additional insured status, or project specifics.

- The certificate holder: The business or person the certificate is issued to, the one who asked you for proof.

What a certificate is NOT

This is where costly misunderstandings start. A certificate of liability insurance is not an insurance policy, and it carries less power than people assume:

- It does not change your coverage. The certificate only reports what your policy already says. If the policy doesn’t cover something, neither does the certificate.

- It does not create rights for the recipient. By itself, the certificate gives the certificate holder no ability to make a claim against your policy.

- It is a snapshot in time. It reflects your coverage on the day it was issued. If you cancel a policy the next week, the certificate still looks valid but no longer reflects reality.

In short, the policy forms and endorsements control what is actually covered. The certificate is evidence, not protection. The Insurance Information Institute’s primers on commercial coverage reinforce the same point: always look past the summary to the policy itself.

Certificate holder vs. additional insured

If you remember one thing from this guide, make it this distinction. It is the difference between a piece of paper and actual protection, and it trips up business owners and the people who hire them every day.

| Certificate holder | Additional insured | |

|---|---|---|

| What it is | The party who receives the certificate as proof coverage exists | A party actually added to your policy by endorsement |

| Rights under your policy | None by itself | Granted defense and indemnity for claims from your operations |

| How it’s created | Just by being named on the certificate | Requires a policy endorsement (and usually a fee) |

| Typical cost | Free | About $50 to $200 per year |

Here’s the trap: being listed as a certificate holder does not automatically make someone an additional insured. A contractor who only asks to be the certificate holder gets proof you’re insured, but no coverage under your policy if they’re sued over your work. To actually be protected, they need to be named as an additional insured by endorsement, which extends your policy’s defense and indemnity to them for claims arising from your operations. When a contract says “name us as additional insured,” a certificate listing them only as the holder does not satisfy it, and people discover the gap at the worst possible moment, after a claim.

How to get a certificate

Getting a certificate is usually quick and painless, as long as one thing is true first: you need an active policy. You can’t produce a valid certificate without coverage actually in force. Assuming you’re insured, the process is simple:

- Ask your agent, broker, or carrier. Request an ACORD 25 from whoever sold you the policy, or generate it yourself if your carrier has an online portal.

- Provide the certificate holder’s details. You’ll need the exact legal name and address of the party requesting it, plus any contract or project reference.

- Specify any endorsements. If the contract requires additional insured or waiver of subrogation status, say so up front, since those change the paperwork.

- Receive and forward it. Check it for accuracy, then send it to whoever asked.

Timing depends on complexity. Most agents issue a standard certificate within 24 to 48 hours, and agencies with online portals can generate a basic one almost instantly. If your request needs endorsements added to the policy, allow 5 to 7 business days for the carrier to process them.

What it costs

The good news: the certificate itself is usually free, or no more than a nominal fee in the $0 to $50 range. What costs money are the endorsements some contracts require, because those actually modify your policy. According to commercial-insurance pricing data compiled by industry sources such as Insureon, typical ranges are:

- Additional insured endorsement: about $50 to $200 per year.

- Waiver of subrogation: about $50 to $150.

- Primary and non-contributory wording: about $100 to $300.

It’s worth budgeting for these when you bid on contracts that demand them, since a client requiring all three can add a few hundred dollars a year to your premium. For a fuller picture of what business coverage costs, see our guide to the best small business insurance.

Why businesses ask for one

Understanding who asks for proof, and why, helps you anticipate the requirement instead of scrambling when a deal is on the line. The demand almost always comes down to one party wanting to shift risk away from itself:

- Landlords and property managers require proof before leasing commercial space, so that if a customer slips in your shop, your coverage responds, not theirs.

- General contractors won’t let a subcontractor on a job site without it, both to protect the project and because their own insurer demands it.

- Corporate and government clients make it a condition of signing, often with specific limit and endorsement requirements written into the contract.

- Vendors and event venues ask for it before you set up at a market, a venue, or a trade show.

- Lenders and franchisors may require ongoing proof as a condition of financing or a franchise agreement.

In every one of these cases, the request is really a question: “If your work causes a loss, will your insurance pay, so I don’t have to?” The certificate answers that question in a format the asking party’s own risk managers trust. Anticipating it, and keeping a current copy ready to send, makes you look professional and keeps deals moving.

Certificates for common situations

The same form shows up in slightly different ways depending on your work, and knowing the pattern saves back-and-forth:

- Subcontractors: Expect the general contractor to require additional insured status and often primary and non-contributory wording, not just a plain certificate. Read the subcontract’s insurance section before you bid.

- Commercial tenants: Landlords usually want the building owner and the management company both named, and a specific liability limit that matches the lease.

- One-off events: Many venues require a certificate naming them for the single day, which a short-term or event policy can supply.

- Ongoing client contracts: Larger clients may ask for a fresh certificate at each renewal, so the proof never goes stale.

The lesson across all of them: read the insurance clause of any contract before you sign it, so the certificate you order matches exactly what’s required. A mismatch, like a certificate listing the client as holder when the contract demands additional insured status, can stall a project or void a key protection.

How to read and verify one

When you receive a certificate from a vendor or subcontractor, don’t just file it. A quick check protects you:

- Are the dates current? Confirm the policies haven’t expired. An out-of-date certificate is worthless.

- Are the limits high enough? Compare the per-occurrence and aggregate limits against what your contract requires.

- Are the right coverages listed? A job may require general liability, auto, and workers’ comp, not just one.

- Are you actually an additional insured? If your contract requires it, check that the description box says so, don’t settle for being only the certificate holder.

- Does the named insured match? The business name on the certificate should match the company you actually hired.

If anything looks off, ask for a corrected certificate before work begins. For higher-risk professional work, you may also want to confirm separate coverages like our guide on errors and omissions insurance describes. And remember that ACORD, which standardizes the forms and the glossary maintained by insurers like Insureon, both stress the same caution: the certificate summarizes, the policy governs.

When a certificate is wrong or expires

Certificates aren’t “set and forget.” Because each one is a snapshot tied to specific policy dates, a certificate that was perfect in January can be meaningless by the time a claim happens in December. Two situations come up constantly.

When yours is about to expire. Every certificate carries the expiration dates of the underlying policies. The party holding it, your client or landlord, often tracks those dates and will ask for a renewed certificate when your policy renews. The smoothest approach is to have your agent reissue updated certificates to your regular holders as soon as you renew, before anyone has to chase you. A lapse in proof can technically put you in breach of a contract even if your coverage never actually stopped.

When one you received is wrong. If a subcontractor sends you a certificate with expired dates, limits below your contract’s requirement, or your company missing from the additional insured line, don’t accept it and hope. Send it back and ask for a corrected version before the work starts. It feels awkward, but a five-minute correction up front is far cheaper than discovering after an accident that you were never actually protected. Keep a simple log of who owes you a current certificate and when each expires; many businesses track this in a spreadsheet or with certificate-tracking software so nothing slips through.

The underlying principle is the same one that runs through this whole topic: the certificate is only as good as the live policy behind it, on the day you actually need it. Treat it as a living record, not a one-time formality, and it does its job.

Frequently asked questions

How much does a certificate of liability insurance cost?

The certificate itself is usually free or up to about $50. The costs come from endorsements a contract may require: an additional insured endorsement runs about $50 to $200 per year, a waiver of subrogation about $50 to $150, and primary and non-contributory wording about $100 to $300.

How long does it take to get a certificate of insurance?

Most agents issue a standard certificate within 24 to 48 hours, and online carrier portals can generate a basic one almost instantly. If the request requires adding endorsements to your policy, allow 5 to 7 business days.

Is a certificate holder the same as an additional insured?

No, and the difference matters. A certificate holder simply receives proof that your insurance exists and has no rights under your policy. An additional insured is added to your policy by endorsement and actually receives defense and indemnity coverage. Being a certificate holder does not make someone an additional insured.

Does a certificate of liability insurance prove I’m covered for a specific claim?

Not on its own. The certificate proves a policy existed on the issue date and summarizes its limits, but the actual policy forms and endorsements determine whether any specific claim is covered. Always look to the policy, not just the certificate.

Do I need a new certificate every year?

Usually yes if a client or landlord keeps you on file. Because each document is tied to your policy’s effective and expiration dates, it goes stale when the policy renews. Many businesses ask their agent to automatically reissue updated copies to regular holders at each renewal, so proof never lapses and no one has to chase it.

What’s the difference between a COI and an insurance policy?

A COI, the common shorthand for this document, is a one-page summary that proves a policy exists and lists its limits and dates. The policy is the full legal contract that actually determines what is covered. The summary reports; the contract governs. Always rely on the policy for any question about whether a specific loss is covered.

Can I make a claim against a company because I’m their certificate holder?

No. Being a certificate holder gives you no right to claim against the policy. Only a named insured or a properly added additional insured can seek coverage. If you need protection under another party’s policy, you must be added as an additional insured by endorsement.

The bottom line

A certificate of liability insurance is simple once you see it clearly: a standardized ACORD 25 summary that proves a business carries coverage, usually free to obtain, and issued within a day or two by your agent. But it is evidence, not protection. The certificate doesn’t change coverage or grant rights by itself, and being listed as the certificate holder is not the same as being an additional insured, the distinction that decides whether anyone is actually covered. Know what’s on the form, ask for the endorsements your contracts require, and verify every certificate you receive. Keep current copies on file for the clients and landlords who need them, and reissue them the moment your policy renews. Do all of that, and a request to “send a COI” becomes a routine two-minute task instead of a source of hidden risk, and you become the rare business owner who actually understands the document everyone else just forwards.

Sources: ACORD, standardized insurance forms (ACORD 25); Insurance Information Institute, commercial coverage basics; Insureon, Certificate of Liability Insurance glossary.